Case Study

Schuler

G. The cause and effects of the change in standard economic policies from the turn of the 19th century through the modern era.

Economics over time: Pre 19th centuryTwo groups, later called "mercantilists" and "physiocrats", directly influenced the subsequent development of the ecomonics and economic theory in the modern era. Both groups were associated with the rise of economic nationalism and modern capitalism in Europe. Mercantilism was an economic doctrine that flourished from the 16th to 18th century. Mercantilism states that a nation's wealth depended on its accumulation of gold and silver. Nations without access to mines could obtain gold and silver from trade only by selling goods abroad and restricting imports other than of gold and silver. The doctrine called for importing cheap raw materials to be used in manufacturing goods, which could be exported, and for state regulation to impose protective tariffs on foreign manufactured goods and prohibit manufacturing in the colonies. Physiocrats, a group of 18th century French thinkers and writers, developed the idea of the economy as a circular flow of income and output. Physiocrats believed that only agricultural production generated a clear surplus over cost, so that agriculture was the basis of all wealth. Thus, they opposed the mercantilist policy of promoting manufacturing and trade at the expense of agriculture, including import tariffs. Physiocrats advocated replacing administratively costly tax collections with a single tax on income of land owners. In reaction against copious mercantilist trade regulations, the physiocrats advocated a policy of laissez-faire, which called for minimal government intervention in the economy. .

MarxismThe Marxist school of economic thought comes from the work of German economist Karl Marx. Marxist (later, Marxian) economics descends from classical economics. It derives from the work of Karl Marx. The first volume of Marx's major work, Das Kapital, was published in German in 1867. In it, Marx focused on the labour theory of value and the theory of surplus value which, he believed, explained the exploitation of labour by capital. The labour theory of value held that the value of an exchanged commodity was determined by the labour that went into its production and the theory of surplus value demonstrated how the workers only got paid a proportion of the value their work had created.

Keynesian EconomicsKeynesian economics and Post-Keynesian economics John Maynard Keynes (right), was a key theorist in economics. Keynesian economics derives from John Maynard Keynes, in particular his book The General Theory of Employment, Interest and Money (1936), which ushered in contemporary macroeconomics as a distinct field. The book focused on determinants of national income in the short run when prices are relatively inflexible. Keynes attempted to explain in broad theoretical detail why high labour-market unemployment might not be self-correcting due to low "effective demand" and why even price flexibility and monetary policy might be unavailing. Such terms as "revolutionary" have been applied to the book in its impact on economic analysis.Keynesian economics has two successors. Post-Keynesian economics also concentrates on macroeconomic rigidities and adjustment processes. Research on micro foundations for their models is represented as based on real-life practices rather than simple optimizing models. It is generally associated with the University of Cambridge and the work of Joan Robinson.

New-Keynesian economics is also associated with developments in the Keynesian fashion. Within this group researchers tend to share with other economists the emphasis on models employing micro foundations and optimizing behavior but with a narrower focus on standard Keynesian themes such as price and wage rigidity. These are usually made to be endogenous features of the models. |

Adam Smith: The Beginning of the Modern EraModern economic analysis is customarily said to have begun with Adam Smith (1723–1790). Smith was harshly critical of the mercantilists but described the physiocratic system "with all its imperfections" as "perhaps the purest approximation to the truth that has yet been published" on the subject.

Adam Smith wrote The Wealth of Nations Publication of Adam Smith's The Wealth of Nations in 1776, has been described as "the effective birth of economics as a separate discipline." The book identified land, labor, and capital as the three factors of production and the major contributors to a nation's wealth, as distinct from the Physiocratic idea that only agriculture was productive. Smith discusses potential benefits of specialization by division of labour, including increased labour productivity and gains from trade, whether between town and country or across countries. His "theorem" that "the division of labor is limited by the extent of the market" has been described as the "core of a theory of the functions of firm and industry" and a "fundamental principle of economic organization To Smith has also been ascribed "the most important substantive proposition in all of economics"

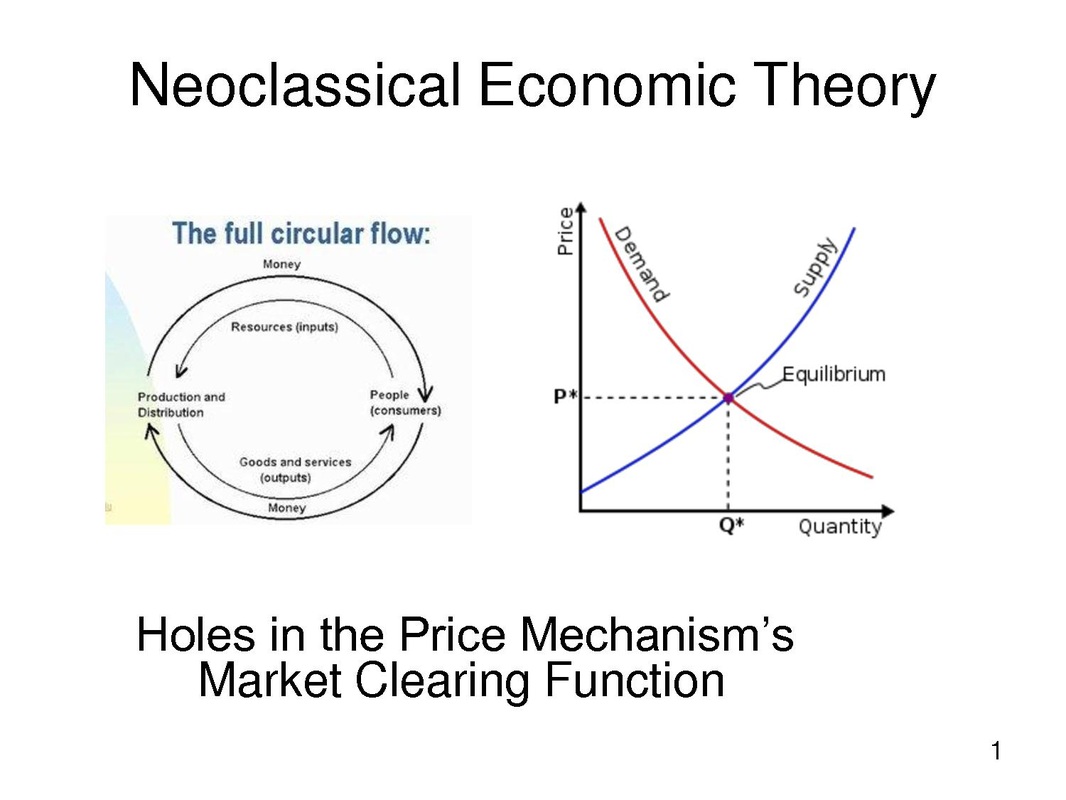

The Modern Era: 1800 - Today:Neoclassical EconomicsA body of theory later termed "neoclassical economics" or "marginalism" formed from about 1870 to 1910. The term "economics" was popularized by such neoclassical economists as Alfred Marshall as a concise synonym for 'economic science' and a substitute for the earlier "political economy". This corresponded to the influence on the subject of mathematical methods used in the natural sciences.

Neoclassical economics systematized supply and demand as joint determinants of price and quantity in market equilibrium, affecting both the allocation of output and the distribution of income. It dispensed with the labour theory of value inherited from classical economics in favor of a marginal utility theory of value on the demand side and a more general theory of costs on the supply side.[130] In the 20th century, neoclassical theorists moved away from an earlier notion suggesting that total utility for a society could be measured in favor of ordinal utility, which hypothesizes merely behavior-based relations across persons.In microeconomics, neoclassical economics represents incentives and costs as playing a pervasive role in shaping decision making. An immediate example of this is the consumer theory of individual demand, which isolates how prices (as costs) and income affect quantity demanded. In macroeconomics it is reflected in an early and lasting neoclassical synthesis with Keynesian macroeconomics.Neoclassical economics is occasionally referred as orthodox economics whether by its critics or sympathizers. Modern mainstream economics builds on neoclassical economics but with many refinements that either supplement or generalize earlier analysis, such as econometrics, game theory, analysis of market failure and imperfect competition, and the neoclassical model of economic growth for analyzing long-run variables affecting national income.

|